10 Key Insights Into Whether Mortgage Rates Will Go Down

One of the most common questions from homebuyers, refinancers, and homeowners is this:

Would the mortgage rates go down soon?

Given how dramatically mortgage rates climbed in recent years—and how deeply those changes impact your monthly payments, affordability, and financial planning—understanding where interest rates might head is essential.

In this comprehensive guide, we’ll explore whether mortgage rates are likely to go down in 2026 and beyond, what’s driving rate trends, how experts forecast future moves, and what this all means for you. We’ll also include easy‑to‑read tables, insights from economists, and a detailed FAQs section.

Let’s dive in.

1. Current Mortgage Rate Environment (2026 Snapshot)

Before answering would the mortgage rates go down, it’s important to know where they stand today.

As of mid‑April 2026, mortgage rates have moved slightly downward from recent highs but still sit elevated compared to historical averages. Recent data shows:

-

30‑year fixed mortgage rates averaging around the mid‑6% range — roughly 6.20%–6.40%.

The Wall Street Journal -

15‑year fixed mortgage rates tend to run lower, often near 5.7%–5.8%.

The Wall Street Journal

Mortgage rates briefly dipped but have been volatile due to inflation, global uncertainty, and economic data. Experts broadly describe rates as remaining relatively high—but with room for gradual eases rather than sharp drops.

2. What Drives Mortgage Rates: The Key Factors

To understand whether mortgage rates will go down, you must understand what affects them in the first place.

A. Federal Reserve Policy

Mortgage rates are influenced by monetary policy—especially the Federal Reserve’s decisions about short‑term interest rates. While the Fed doesn’t directly set mortgage rates, its actions affect the broader credit and bond markets.

Key Points:

| Driver | How It Impacts Rates |

|---|---|

| Fed rate cuts | Can lower borrowing costs but not always mortgage rates directly |

| Fed rate hikes | Often push mortgage rates higher |

| Neutral stance | Often leads to stable or slightly lowering mortgage rates |

Lower inflation often gives the Fed room to cut rates, which indirectly helps mortgage rates decline.

B. Inflation and Economic Data

Inflation remains one of the most important trends shaping mortgage rates. If inflation comes down toward the Fed’s target (around 2%), long‑term rates—including mortgage rates—have more room to fall.

A slowing economy or weaker inflation data typically reduces upward pressure on mortgage rates, potentially pushing them down over time.

C. The 10‑Year Treasury Yield

Mortgage rates are heavily tied to the yield on the 10‑year U.S. Treasury note. When the yield rises, mortgage rates tend to rise as well; when it falls, mortgage rates often follow.

Put simply:

Mortgage rates ≈ 10‑Year Treasury Yield + Spread + Lender Costs

So if treasury yields decline due to slower growth or risk‑off investor behavior, mortgage rates can follow.

3. Expert Forecasts: Would the Mortgage Rates Go Down?

When evaluating would the mortgage rates go down, multiple expert forecasts help provide perspective.

A. Consensus Forecasts for 2026

Several major institutions have shared their outlooks:

| Forecast Source | Prediction for 2026 |

|---|---|

| Morgan Stanley | Rates may fall to ~5.50%–5.75% mid‑2026, then rise later.

Morgan Stanley

|

| Fannie Mae, MBA, NAR Consensus | Rates slowly down, average 5.8%–6.3%.

Mortgage-Info.com

|

| Bankrate Average | ~6.1% average for 2026.

Bankrate

|

| Redfin & Realtor.com | Moderately lower, but rates remain elevated.

Money

|

Most economists agree that mortgage rates might decline moderately through 2026—especially in the second half of the year—but a steep drop back to pandemic‑era levels (like 3%–4%) is unlikely in the short term.

4. Timeline of Expected Mortgage Rate Changes

Here’s a broad look at how rates might evolve through the year:

| Time Period | Expected Mortgage Rate Trend | Explanation |

|---|---|---|

| Early 2026 | High but slightly easing (~6.2%–6.5%) | Slow decrease from previous peaks as inflation cools.

Mortgage-Info.com

|

| Mid‑2026 | Gradual decline continues (~6.0%–6.3%) | Fed rate cuts begin impacting bonds.

Mortgage-Info.com

|

| Late 2026 | Best potential rates (~5.5%–5.9%) | Inflation pressure eases, yields fall.

Mortgage-Info.com

|

The biggest declines are expected later in 2026, typically in the 3rd and 4th quarters.

5. What Would Make Mortgage Rates Go Down?

Now that we’ve looked at forecasts, let’s break down the conditions that could actually push mortgage rates lower.

A. Lower Inflation

Mortgage rates tend to fall when inflation is under control since the Federal Reserve doesn’t need to maintain tight monetary policy. A consistent drop toward the Fed’s target could reduce borrowing costs for lenders, and therefore consumers.

B. Federal Reserve Cuts

If the Fed cuts the federal funds rate, this can indirectly influence mortgage rates over time. Cuts often signal that policymakers see slower economic growth ahead, which usually leads to modest reductions in mortgage rates.

Experts predict multiple possible rate cuts in 2026 if inflation keeps trending downward.

C. Economic Slowdown Without Recession

An economy that slows without tipping into recession often sees safe‑haven demand for long‑term bonds increase. That demand pushes Treasury yields down, which in turn can lower mortgage rates.

D. Global Economic Conditions

International uncertainty can drive investors into U.S. bonds, lowering yields and lending rates. For instance, geopolitical stress or global market weakness often increases bond prices, reducing yields—and sometimes mortgage rates follow.

6. What Wouldn’t Make Them Go Down

On the flip side, several forces could stop or reverse declines in mortgage rates:

| Factor | How It Prevents Rates From Falling |

|---|---|

| Persistent Inflation | Keeps upward pressure on long‑term rates |

| Strong Job Market | Encourages consumer spending and higher rates |

| Tight Housing Market | Encourages competition and maintains higher spreads |

| Fiscal Pressure (Government Deficits) | Can keep yields elevated despite rate cuts

New York Post

|

In other words, even if inflation cools, strong economic data or fiscal pressure can keep mortgage rates above decline thresholds.

7. How Much Could Rates Actually Fall?

Experts generally do not expect mortgage rates to plummet to ultra‑low levels.

Typical projections for 2026 include:

-

Moderate declines — e.g., 5.5%–5.9% by late 2026.

Mortgage-Info.com -

Stable ranges near current levels — around 6.1%.

Bankrate -

Low risk of dramatic drops below 5% in 2026.

Money

Averages may vary by region or lender, but overall forecasts suggest a gradual descent rather than sharp movement.

8. Will Mortgage Rates Go Down in the Long Term (Beyond 2026)?

Looking farther ahead into the late 2026–2027 window, a few economists predict a modest downward trend continues:

-

Some projections suggest rates could stabilize around 5.5%–5.7% range by 2027 if inflation continues to fall.

Mortgage-Info.com -

However, other forecasts see rates hovering near 6.2% long term without major economic shifts.

Reddit -

A more pessimistic forecast even expects rates could stay above 6% through 2028 due to structural factors like deficits and higher yields.

Reddit

In short, long‑term declines are possible but not guaranteed and depend on many economic variables.

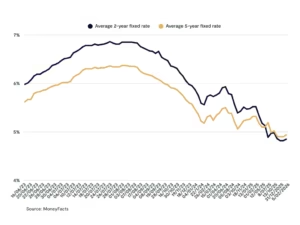

9. Historical Context: Why Current Rates Feel High

To understand why people constantly ask would the mortgage rates go down, it’s useful to look at recent history:

| Period | Average 30‑Year Rate |

|---|---|

| 2020–2021 | Around 2.5%–3.5% (record lows) |

| 2022 | Jumped above 5% |

| 2023 | Climbed above 7% |

| 2024–2025 | Remained elevated (~6%+) |

| 2026 | Mid‑6% range currently |

This context shows how unusual the ultra‑low rates of the pandemic period were. Returning to those levels is not expected anytime soon.

10. How This Affects Your Homebuying or Refinancing Strategy

So would the mortgage rates go down enough to change your plans?

Here are key considerations:

A. Don’t Wait Forever

If you’re hoping for perfect rates, keep in mind:

-

Forecasts are not guarantees.

-

Waiting for marginal rate decreases might delay your homeownership or refinance goals.

Mortgage-Info.com

B. Plan Around Your Financial Goals

Consider locking in a rate that works with your budget rather than banking on future changes.

C. Refinancing Later Is an Option

Even if you buy at today’s rates, you can refinance later if rates decline meaningfully.

Mortgage Rate Trends: Quick Comparison Table

| Year | Typical 30‑Year Mortgage Rate |

|---|---|

| 2022 | ~6%–7.8% |

| 2023 | ~7% |

| 2024 | ~6.5% |

| 2025 | ~6.2% |

| 2026 (forecast) | ~5.5%–6.3% |

| 2027 (possible) | ~5.5%–6.0% |

This table illustrates a potential gradual downward drift but not a dramatic return to sub‑5% rates.

Frequently Asked Questions (FAQs)

Q1: Would the mortgage rates go down in 2026?

Most forecasts suggest mortgage rates will gradually decrease through 2026, possibly easing into the 5.5%–5.9% range by late in the year.

Q2: What drives mortgage rates lower?

Falling inflation, Federal Reserve rate cuts, weaker treasury yields, and slowing economic activity tend to push rates down.

Q3: Could mortgage rates go back to 3%–4%?

Experts generally agree such low rates are unlikely in the near future without dramatic economic shifts.

Q4: Should I wait to buy for lower mortgage rates?

Waiting can work if rates fall significantly, but small declines may not outweigh other factors like home price increases.

Q5: How frequently do mortgage rates change?

Mortgage rates change daily based on market conditions, economic data, inflation reports, and bond yields.

Q6: Do Fed cuts always lead to mortgage rate declines?

Not always; mortgage rates don’t move in lockstep with the Fed’s policy rate, but cuts often put downward pressure on long‑term borrowing costs.

Q7: Can refinancing help if rates drop?

Yes — if mortgage rates decline enough, refinancing can save money on monthly payments or the total cost of your loan.

Final Takeaway

So would the mortgage rates go down? The answer isn’t a simple yes or no — it’s nuanced:

-

Mortgage rates are likely to move down gradually through 2026.

Mortgage-Info.com -

A dramatic return to pandemic‑era lows is unlikely.

Money -

The largest declines may occur later in the year if inflation cools and the Fed cuts rates.

Mortgage-Info.com